Supervised learning¶

We are given training data $(X, Y) = \{(x_1, y_1 ),\cdots , (x_N, y_N )\}$

- X: independent variables, inputs, predictors, features

- Y: dependent variables, outputs, response

$x \in \mathbb{R}^P$ (usually)

- regression: $y \in \mathbb{R}$

- classification: $y \in \{0, 1\}$

- structured prediction: More complicated high-dimensional spaces with dependent components (e.g. the space of images or sentences)

We assume $y_i = f(x_i ) + \varepsilon_i$

$\varepsilon$ is noise (includes randomness and approximations)

- Independently and identically distributed (i.i.d.) according to some probability distrib. (e.g. Gaussian)

Given the training set $(X, Y)$, we want to estimate $f$:

- to study the relation between x and y

- to make predictions of y’s for unobserved x’s

Good predictors can be hard to interpret

Parametric learning¶

Index functions $f$ by a finite-dimensional parameter vector

E.g. linear regression

- Parameters are coefficients of a hyperplane

- Parameters have a clear interpretation

- Can be a bad approximation of reality

Linear regression¶

via the lm function in R

library('ggplot2')

DataIncm <- read.table('Data/Income2.csv',header=T,sep=',')

ggplot(DataIncm) + geom_point(aes(x=Education,y=Income))

fit <- lm(Income ~ Education, DataIncm); fit

The first argument is a formula

- takes the form response ~ predictors

- response is a linear combination of predictors

- above we have just one predictor: $Education$

- $Income = \beta_1 \cdot Education + \beta_0 + \epsilon$

Second argument unnecessary if variables in formula exist in current environment

See documentation for other optional arguments

Can print fit:

fit

This is not all the information in fit (why?)

- Try

typeof(),class(),str() - Try plotting it

print.default(fit)

Observe fit contains the entire dataset!

Can disable with model = FALSE option

Can directly plot with ggplot :

plt1 <- ggplot(DataIncm, aes(x=Education, y = Income)) +

geom_point(size=2, color='blue') +

theme(text=element_text(size=10))

plt1 + geom_smooth(method='lm', se=FALSE, #Disable std. errors

color='magenta', size=2)

Can regress against Seniority

fit <- lm(Income ~ Seniority, DataIncm)

Can regress against both Education and Seniority

fit <- lm(Income ~ Education + Seniority, DataIncm)

+does not mean input is sum of Educ. and Sen.

Rather: $Income = \beta_2 \cdot Seniority + \beta_1 \cdot Education + \beta_0 + \varepsilon$

For the former, use I:

fit <- lm(Income ~ I(Education + Seniority), DataIncm)

- $Income = \beta_1 \cdot (Seniority + Education) + \beta_0 + \varepsilon$

Prediction¶

fit <- lm(Income ~ Education + Seniority, DataIncm)

How do we make predictions at a new set of locations? E.g. (15, 60) and (20, 160)?

pred_locn <- data.frame(Education=c(15,20), Seniority= c(60,160))

predict.lm(fit, pred_locn)

edu_pred <- 10:25

sen_pred <- seq(0,200,10)

pred <- data.frame(Education=rep(edu_pred, length(sen_pred)),

Seniority=rep(sen_pred, each=length(edu_pred) ))

p_val <- predict.lm(fit, pred)

pred$p_val = p_val

plt <- ggplot(DataIncm, aes(x=Education, y=Seniority,

color=Income))+

geom_tile(data=pred, aes(x=Education, y=Seniority,

color=p_val, fill=p_val)) +

geom_point(size=1) + theme(text=element_text(size=10)) +

scale_color_continuous(low='blue', high='red') +

scale_fill_continuous(low='blue', high='red') +

geom_point(shape=1,size=1,color='black') +

guides(fill=FALSE) # Remove legend for 'fill'

plt

Specifying a model for lm

| Symbol | Meaning | Example |

|---|---|---|

| + | Include variable | x + y |

| : | Interaction between vars | x + y + z + x:z + y:z |

| * | Variables and interactions | (x + y) * z |

| ^ | Vars and intrcns to some order | (x + y + z)^3 |

| - | Delete variable | (x + y + z)^3 - x:y:z |

| poly | Polynomial terms | poly(x,3) + (x + y) * z |

| I | New combination of vars | I(x*y + z) |

| 1 | Intercept | x - 1 |

See documentation and http://ww2.coastal.edu/kingw/statistics/R-tutorials/formulae.html

Generalized linear model¶

A linear model with Gaussian noise is often inappropriate. E.g.

- response is always positive

- count valued response

- {0, 1} or binary-valued as in classification

A better model might be:

$ response = g (\sum_{i=1}^N \beta_i \cdot predictor_i) + \varepsilon$

$g$ is a ‘link’ function, $\varepsilon$ is no longer Gaussian

Can fit in R with glm() (see documentation)

Nonparametric methods¶

No longer limit yourself to a parametric family of functions

Much more flexible

Often much better prediction

Complexity of $f$ can grow with size of dataset

Often hard to interpret

k-nearest neighbors¶

Given training data $(X, Y)$

Given a new $x^∗$ , what is the corresponding $y^∗$?

Find the k-nearest neigbours of $x^∗$ . Then:

- Classification: Predicted $y^∗$ is the majority class-label of the neighbors

- Regression: Predicted $y^∗$ is the average of the $y$’s of the neighbors

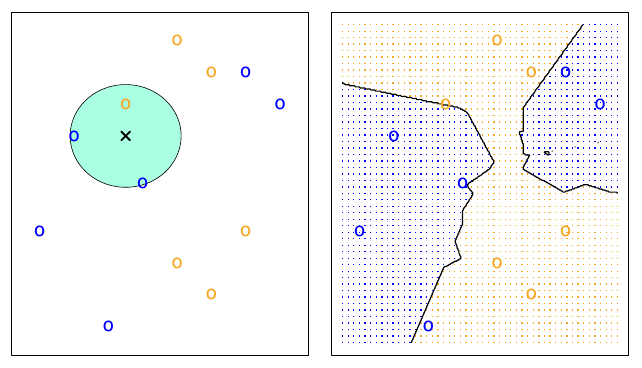

3-nearest neighbors

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

Complexity of decision boundary grows with size of training set: ‘Nonparametric’

Pros:¶

- Very intuitive computational algorithm.

- Very easy to ‘fit’ data (you don’t, you just store it)

- Tends to outperform more complicated models.

- Easy to develop more complicated extensions E.g. locally-adaptive kNN.

- Exists theory for such models.

Cons:¶

- Cost of prediction grows linearly with training set size (can be expensive for large datasets)

- Tends to break down in high-dimensional spaces.

- Exempler-based approaches are hard to interpret.

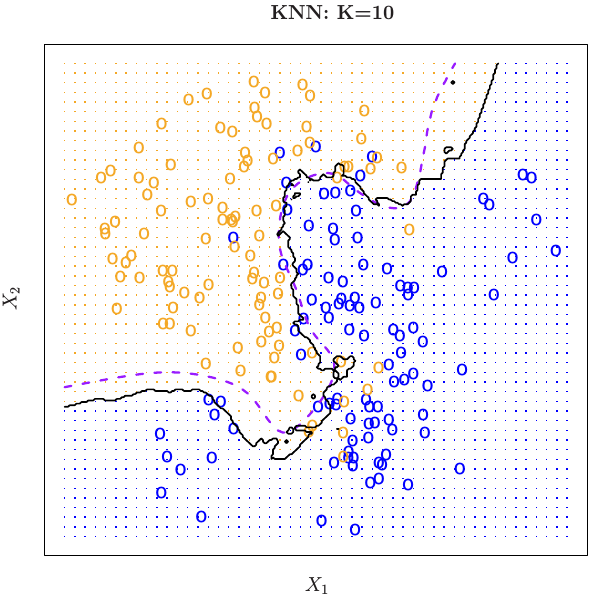

10-nearest neighbors

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

- What distance function do we use? Typically Euclidean.

- What k do we use? Typically 3, 5, 10

Usually chosen by cross-validation (more later)

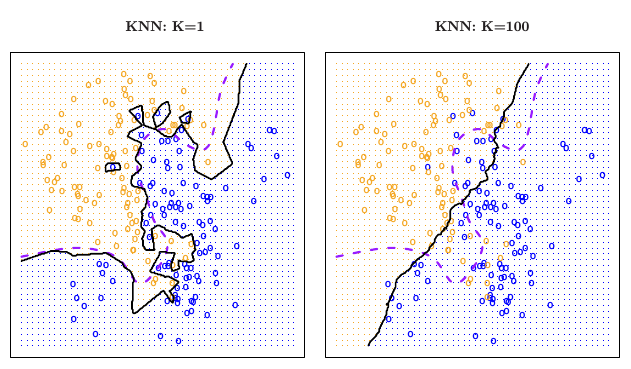

Large k: smooth decision boundary

Small k: complex decision boundary (with local variations)

- k is a measure of model-complexity

How do we perform model selection?

Do we prefer simple or complex models?

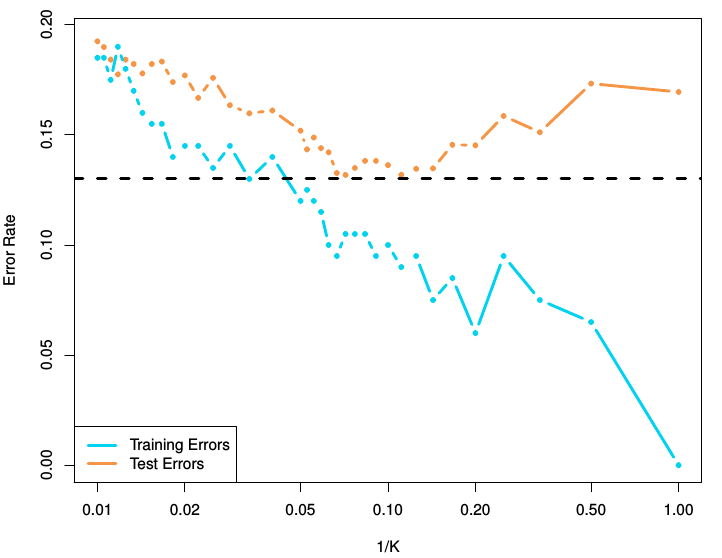

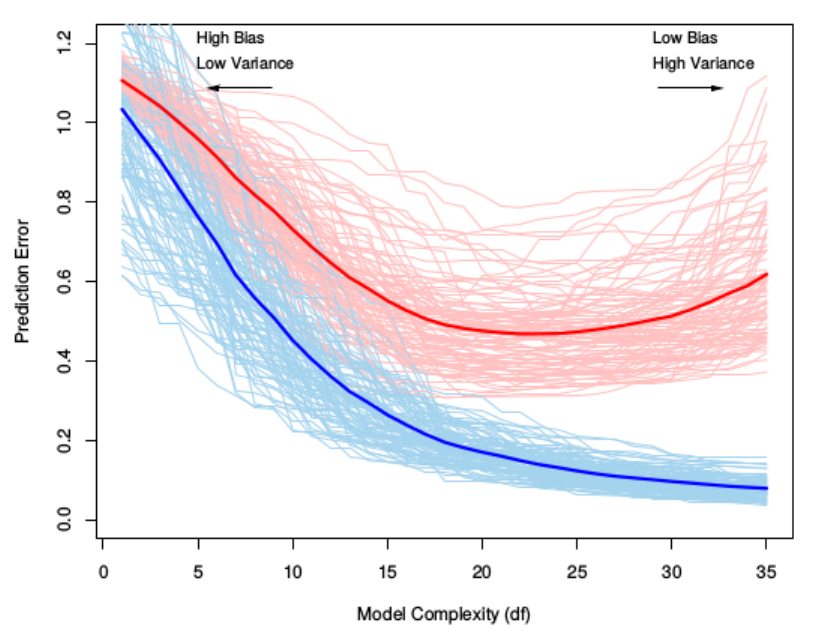

Bias-variance trade-off¶

Overly simple models

- cause underfitting (or bias)

- ignore important aspects of training data

Overly complex models

- cause overfitting (or variance)

- can be overly sensitive to noise in training data

Complex models reduce training error, but generalize poorly.

Cross-validation¶

How do we estimate generalization ability? Create an unseen test dataset.

Cross-validation:

- Split your data into two sets, a training and test dataset.

- Fit all models on training set.

- Evaluate all models on test set.

- Pick best model.

Choosing k by cross-validation¶

Often 50-50 or 70-30 training-test splits are used

Too small a test set:

- Noisy estimates of generalization error

Too small a training set:

- Wasting training data

- Model selected using small training set may be simpler that model relevant to the entire training set

k-fold crossvalidation¶

Split your data into k-blocks.

For i = 1 to k:

- Fit algorithm on all except block i.

- Test algorithm on block i. Overall generalization error is the average of all errors.

- Can use larger training sets

- Can get confidence intervals on generalization error.

k = N: leave-one-out cross-validation

k-fold crossvalidation¶

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)

(*An Introduction to Statistical Learning*, James, Witten, Hastie and Tibshirani)